HBL Ghar Scheme 2025

Habib Bank Limited (HBL) is one of Pakistan’s largest and most right-hand banks. Through its Islamic and conservative banking arms, HBL offers home financing / housing schemes (occasionally casually called “HBL Ghar”) that aim to help middle and low-income persons buy, build, or renew their homes. Below is a whole guide (A to Z) on how HBL cover economics works in 2025.

Quick Facts Table for HBL Ghar Scheme 2025

| Program / Scheme | Start Date / Launch | End / Deadline* | Assistance / Subsidy / Rate | Application Mode (Online / Offline) |

|---|---|---|---|---|

| HBL Islamic Home Finance (via diminishing musharakah) | Active (2025) | Ongoing | Floating rental rates, fixed rate options (e.g. ~12.50%) | Apply via HBL Islamic branch or online portal |

| HBL Roshan Apna Ghar | Active | Ongoing | Shariah-compliant, for overseas Pakistanis via RDA | Application via HBL’s Roshan Digital / branch network |

*“End date” is not fixed. Schemes usually run indefinitely until changed by HBL / SBP.

What is HBL Home / Islamic Home Finance?

HBL provides Islamic Home Finance under Shariah principles (deprived of interest) via Lessening Musharakah.

In this preparation, the bank and the client jointly own the possessions, and over time the client buys out the bank’s share while paying “rental” on the bank’s residual share.

HBL also has a Roshan Apna Ghar product specially for Overseas Pakistanis below its Roshan Digital Account (RDA) platform, allowing them to get Shariah-compliant housing money from overseas.

Moreover, HBL markets Prestige Home Finance (for higher segments) with conservative or Islamic options.

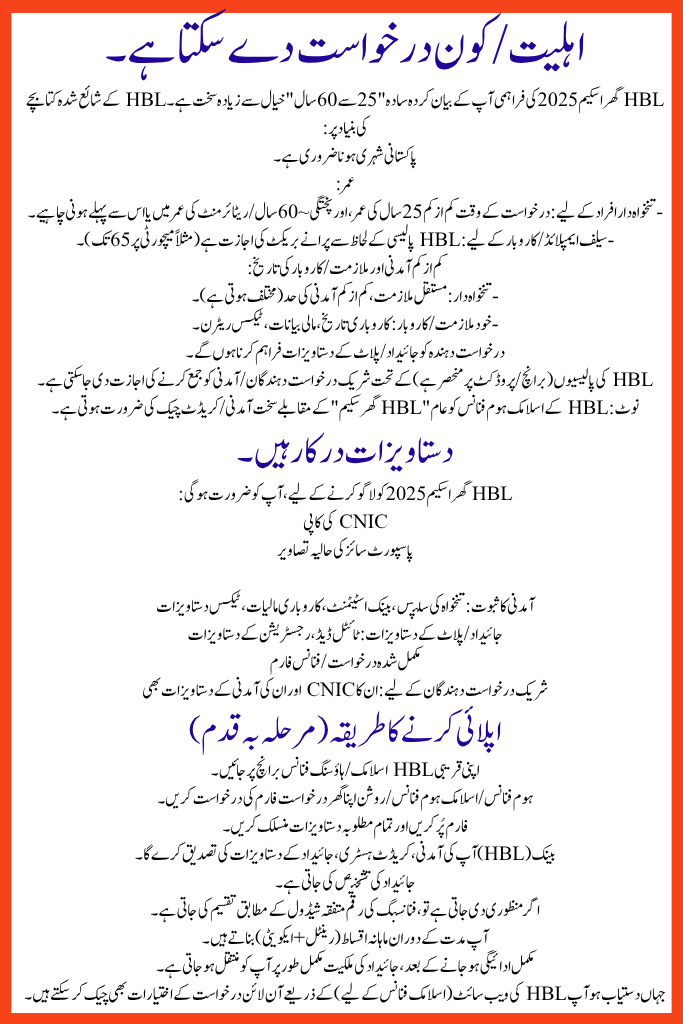

Eligibility / Who Can Apply

HBL Ghar Scheme 2025 supplies are stricter than the simple “25 to 60 years” idea you stated. Based on HBL’s published leaflets:

- Must be a Pakistani citizen.

- Age:

– For salaried persons: at least 25 years old at application, and maturity must fall at or before ~60 years / retirement age.

– For self-employed / business: older bracket allowed (e.g. up to 65 at maturity) depending on HBL policy. - Minimum income and job / business history:

– Salaried: permanent employment, minimum income threshold (varies).

– Self-employed / business: business history, financial statements, tax returns. - Applicant must provide property / plot documents.

- Co-applicant / income clubbing may be allowed under HBL’s policies (depending on branch / product).

Note: HBL’s Islamic Home Finance requires stricter income / credit checks compared to a generic “HBL Ghar scheme.”

Purposes / Uses of the Finance

You can ask HBL Ghar Scheme 2025 to finance:

- Purchase of a ready home / apartment.

- Buy + Build: purchase of land + constructing a house.

- Renovation / Repair / Extension of an existing property.

- Balance Transfer (moving your home loan from another bank to HBL) in some cases (depends on policy).

Loan Amounts, Tenure & Rates

Loan / Financing Amount

- HBL’s Islamic Home Finance backing range is PKR 2,000,000 to PKR 50,000,000 (for certain segments) in their published literature.

- They finance up to 70% of the property value under many of their cover crops.

- For lower-income / backed segments (if applicable), smaller quantities may be allowable.

Tenure (Repayment Period)

- The repayment tenure can range from 3 to 25 years depending on the product.

Rate Structure

- For Islamic Home Finance, HBL offers floating rental rates and fixed rental rates options.

- Example: 12.50% (floating) for one year is mentioned for HBL’s Islamic Home Finance product.

- For Prestige Home Finance, preferential or negotiated rates may apply.

Rates will vary by product, credit score, down payment, and market conditions.

Down Payment / Equity and Customer’s Share

- The customer must provide equity (down payment). In many cases, HBL requires up to 30% down or may finance up to 70% of property value.

- As financing continues, customer’s share in property increases while bank’s share decreases (Diminishing Musharakah).

Documents Required

To apply HBL Ghar Scheme 2025, you will need:

- Copy of CNIC

- Recent passport-size photographs

- Proof of income: salary slips, bank statements, business financials, tax documents

- Property / plot documents: title deed, registration documents

- Completed application / finance form

- For co-applicants: their CNIC and their income documents as well

How to Apply (Step-by-Step)

- Visit your nearest HBL Islamic / housing finance branch.

- Request the home finance / Islamic Home Finance / Roshan Apna Ghar application form.

- Fill the form and attach all required documents.

- Bank (HBL) will verify your income, credit history, property documents.

- Property valuation is performed.

- If approved, the financing amount is disbursed according to agreed schedule.

- You make monthly installments (rental + equity) over the tenure.

- Once full payment is done, the property ownership transfers fully to you.

You may also check for online application options via HBL’s website (for Islamic finance) where available.

Benefits & Advantages of HBL “Ghar / Home Finance”

- Shariah-compliant option (Islamic Home Finance) with no interest.

- Flexible tenures up to 25 years make installments manageable.

- High financing share (up to 70% of property value).

- Many HBL products waive processing or offer discounts under certain segments.

- Available across HBL’s extensive branch network in Pakistan.

- For overseas Pakistanis, Roshan Apna Ghar enables home financing from abroad with HBL.

Things to Watch / Challenges

- Income and credit history inspection is strict — not everybody may qualify.

- Property must meet HBL’s eligibility criteria (location, title, approval).

- Rental / rate changes in floating construction may upsurge payments.

- Down payment requirements may be burdensome for some.

- For high amounts, certification stresses and legal / estimate fees may add up.

Conclusion

“HBL Ghar” or more accurately, HBL Home / Islamic Home Finance is a robust answer for Pakistanis who want to buy, build, or renovate homes under promising terms. Whether you are local or abroad (via Roshan Apna Ghar), HBL offers Shariah-compliant options, flexible tenures, and large financing limits.

Before applying, check eligibility, gather precise leaflets, and visit your nearest HBL subdivision (or use the online portal where obtainable). If you like, I can also produce a monthly instalment calculator for your city and property value under HBL’s scheme to assistance decide.

Related Posts